Passive target-date funds remain a popular choice for many defined-contribution plans, often driven by the generally lower fees associated with these funds. While intuitively it may feel as if “lower cost” naturally translates into a more prudent option for plan participants, the reality is this may not always be the case.

Further, the term “passive TDF” is a little misleading, given that all the decisions made in the construction of TDFs — such as asset class diversification, glide path design, underlying investment strategy selection and portfolio construction — are active decisions. “Passive” only refers to the underlying strategies used to populate these TDFs’ glide paths, which can back them into potentially limiting diversification and glide path decisions that may lower participant outcome potential.

For example, asset classes such as high-yield bonds and real estate – among others – have proven to be difficult or more expensive to replicate as passive strategies, and historically have been extremely additive to long-term performance outcomes. Passive TDF strategies tend to exclude these asset classes as they are more difficult to replicate in an efficient manner.

Exhibit 1: Most passive players are less diversified

Source: Morningstar; data as of 12/31/22. Active managers defined as those with 75%+ actively managed underlying funds; passive managers defined as those with 75%+ passively managed underlying funds. Top five largest active/passive target date fund series as measured by AUM.

Taking these considerations into account, plan fiduciaries and advisors shouldn’t assume that simply selecting a passive TDF automatically lowers their fiduciary risk, or that it’s always the better choice for plan participants.

Here are three reasons.

1. A NEW MARKET CYCLE IS EMERGING

The 10 years prior to 2022 were particularly well suited for passive TDFs. These strategies tend to focus on traditional equities as their primary return engines, particularly large-cap securities, which generally delivered historically impressive returns across that period.

However, 2022 saw that cycle begin to change as rates began to normalize, and broad stock indices suffered their worst declines in years. Though stock market performance has been resilient year-to-date in 2023, we expect the investment climate to continue to place greater importance on correlation diversification to expand return potential and strengthen risk-adjusted performance.

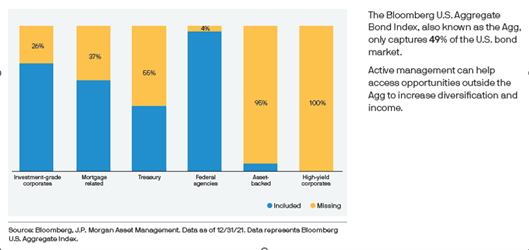

In addition, indexing in fixed income is different than in equities. While the S&P 500 Index captures more than 80% of the stock market, the Bloomberg U.S. Aggregate Bond Index captures only 49% of the bond market and is highly concentrated in Treasuries and agency mortgage-backed securities, excluding many investment-grade securities that are often part of modern, well-diversified portfolios, including approximately 40% of all corporate bonds. As a result, relying only on the index for a TDF’s fixed-income exposure may result in notable opportunity costs and elevated volatility exposures, especially in more challenging investment environments.

Exhibit 2: Indexed core bond strategies may miss more than 50% of the overall market

U.S. core bond market and portion captured by Bloomberg U.S. Aggregate Bond Index

2. The DC LITIGATION LANDSCAPE IS EVOLVING

Lawsuits against DC plan sponsors are nothing new. In the past, most tended to focus on excessive fees. The majority of suits now involve TDFs, and their performance, as well as the potential for performance, is beginning to emerge as a theme.

Recent cases have emphasized performance over fees. Plaintiffs in 11 lawsuits against various plan sponsors all using the same passive TDF as a qualified default investment alternative argue the plan sponsors focused on low fees in strategy selection without considering their ability to generate returns (cases still pending).

An appellate court decision in the second case confirmed that TDF returns should be viewed in context of long-term performance and outcome potential. The court rejected plaintiffs’ claim that recent underperformance of the plan’s active TDF series relative to passive options indicated imprudent strategy selection and monitoring.

It’s important to look deeper into investment performance beyond recent one-, three- and five-year returns when evaluating an investment strategy, especially when the goal is to deliver safer retirement outcomes over a career-spanning investment horizon.

3. THE BEST FIDUCIARY PROTECTION IS A WELL-DEFINED SELECTION AND REVIEW PROCESS

When it comes to prudent TDF selection, it’s not just about price, it’s about process. The Department of Labor’s eight tips for TDF evaluation continue to offer important guidance when selecting an investment

Fees, of course, offer a straightforward, easily quantifiable comparison factor, whereas other guidance factors are more qualitative in nature. However, focusing on fees does not eliminate the other evaluation standards.

CONCLUSION

While selecting a lower-cost, passive TDF may seem like the easy choice, it doesn’t lower a plan’s fiduciary risk on its own. Nor does it eliminate plan fiduciaries’ due diligence and monitoring requirements.

Instead, the focus should be on long-term results:

- Fees are an important consideration but far from the only one: More important criteria include glide path design, the rationale for selecting specific asset classes and underlying investment strategies.

- Consider investment value as well as cost: Evaluate TDF fees in context of a strategy’s net returns over the long term, as well as in shorter-term market environments, to determine how funds have added value in various market environments

It’s not just about returns — it’s about outcomes: Consider how the TDF is likely to affect participants’ investment experience, and how that may be aligned with the plan’s objectives Lastly, remember that the passive/active decision is no longer an either/or choice, with many TDF providers incorporating both into their underlying investment strategies, generally using passive investments to help manage fees while including actively managed investments in asset classes where there may be alpha opportunities. What remains most important is to select a TDF that is well aligned with your plan’s objectives and demographics.

Emily Cao is head of defined contribution investment specialists at J.P. Morgan Asset Management.